As a woman, I am grateful to be born in Singapore where we get equal opportunities.

As a woman, I am grateful to be born in Singapore where we get equal opportunities.

Women today are well educated, capable and taking on more leadership positions.

But when it comes to retirement readiness, we women face a double whammy. Why?

We earn less and have less CPF savings

A 2017 study by NUS Business School found that female directors on Singapore listed companies still earn substantially less than their male counterparts, in some cases as much as 43% lesser. And there exists a pay gap between men and women at other levels too.

Coupled with the fact that almost a quarter of women choose to stop work to care for their children, this means that women generally end up with less CPF savings then men. According to CPF’s 2021 annual report, the average CPF savings of women start to lag behind that of men starting from the ages of 35-45, which ties in with the period when women become mothers.

Yet we live longer and need more money to last us in our retirement

Statistically, women in Singapore have a life expectancy of ~85 years, while men can expect to live to 80. This means as a woman, you’ll need to make sure you prepare enough money to last you for an extra 5 years, plus make up for the lesser savings over the years.

What can women do to boost their retirement funds given these challenges?

Here are 3 financial planning tips that can help

1) Invest your savings – starting as early as possible

Studies show that Singaporean women tend to be good savers, however relying on savings alone can be challenging to meet one’s retirement needs especially in low interest rates environment.

By investing a portion of your savings diligently over the long run, you can grow your wealth and build up your retirement reserves. And the earlier you start, the better, because you have more time for compounding interest to work for you.

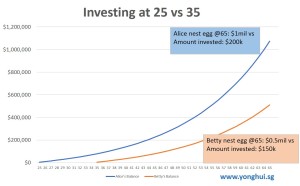

Let’s have a look at two ladies Alice and Betty, both of them invest $5,000/year for their retirement. Alice started earlier at age 25 while Betty only started when she was 35 and they continued to invest until they reached 65.

Assuming an average return of 7% per year, Betty who started at age 35 would end off with an investment nest egg of $500k by age 65 while Alice would have doubled that of Betty with $1million nest egg because of the 10 yrs headstart.

Many women intellectually understand that they should invest but face challenges when it comes to the actual investing. The good news is women can be savvy investors too, find out how you can overcome top 3 mental blocks holding women back and start growing your retirement fund today.

2) Top up your CPF savings

CPF currently provides risk-free interest rates of up to 2.5% for OA and 4% for SA, and the first $60k balances get an additional 1% interest. Increasing your CPF funds helps you earn more interest so you can enjoy higher CPF Life payout during your retirement.

Here are several ways to boost your CPF savings and maximize your interest

- Self top up to your CPF account using cash. You can do a voluntary top up above your mandatory contribution up to the CPF annual limit (currently $37,740)

- Transfer excess funds from your OA to SA to earn higher interest

- For stay home mums, working husbands can do a top up to your CPF account using cash or they can transfer their CPF savings to your Special Account (if you are aged 55 and below) or Retirement Account (if you are above age 55) after setting aside the Basic Retirement Sum (which is $99,400 as of 2023) in their own CPF account. To the hubbies out there, you can treat this as an anniversary gift for your wifey’s future security!

And did I mention that you also save money on taxes by doing cash top ups to your own or loved ones’ SA and/or RA?

You can enjoy dollar for dollar tax relief of up to $8,000 when topping up to your own SA or RA with cash, and an additional tax relief of up to $8,000 for topping up your loved ones’ SA or RA with cash. There’s a pretty good deal to me, so do consider it!

3) Increase Your Income

The last tip is to basically increase the source of funds – your income. Be it you are currently working or not, there are ways to earn more money so you can save more for your retirement.

With technology these days, even home makers can earn some extra income. I know of women who start online blogshops or take on freelance assignments e.g writing, tuition etc to generate extra income for themselves or the family. Some mummies even become successful bloggers who get paid through advertisement or sponsorships.

For those who are currently working, focus on developing your interpersonal skills and expanding your network. Often, it’s not what you know, but who you know that will get you your next better opportunity. Linkedin is a good platform for you to establish yourself, showcase your experience and build your credentials.

Starting a business or becoming an entrepreneur is another way where you can be in control of you own income instead of being limited by income ceilings or gender disparity. Invest in yourself and develop the capabilities to generate recurring earnings through a business.

Starting a business or becoming an entrepreneur is another way where you can be in control of you own income instead of being limited by income ceilings or gender disparity. Invest in yourself and develop the capabilities to generate recurring earnings through a business.

So in a nutshell, to boost your retirement fund – increase your income and make your savings work harder for you by investing and topping up your CPF.

Hope you have found these tips helpful!

- This article was originally published in 2017 and have been updated in 2023 for accuracy and relevancy

To Your Success and Happiness,

Yong Hui